By Joy Balini

When BJP legislature party leader Suvendu Adhikari took oath as Chief Minister of West Bengal on Saturday, heading the state’s first BJP government, the ceremony at Brigade Parade Ground closed one of the longest political cycles in independent India. The Left Front ruled the state from 1977 to 2011; Trinamool Congress from 2011 to 2026. The BJP secured 207 seats in the 294- member Assembly.

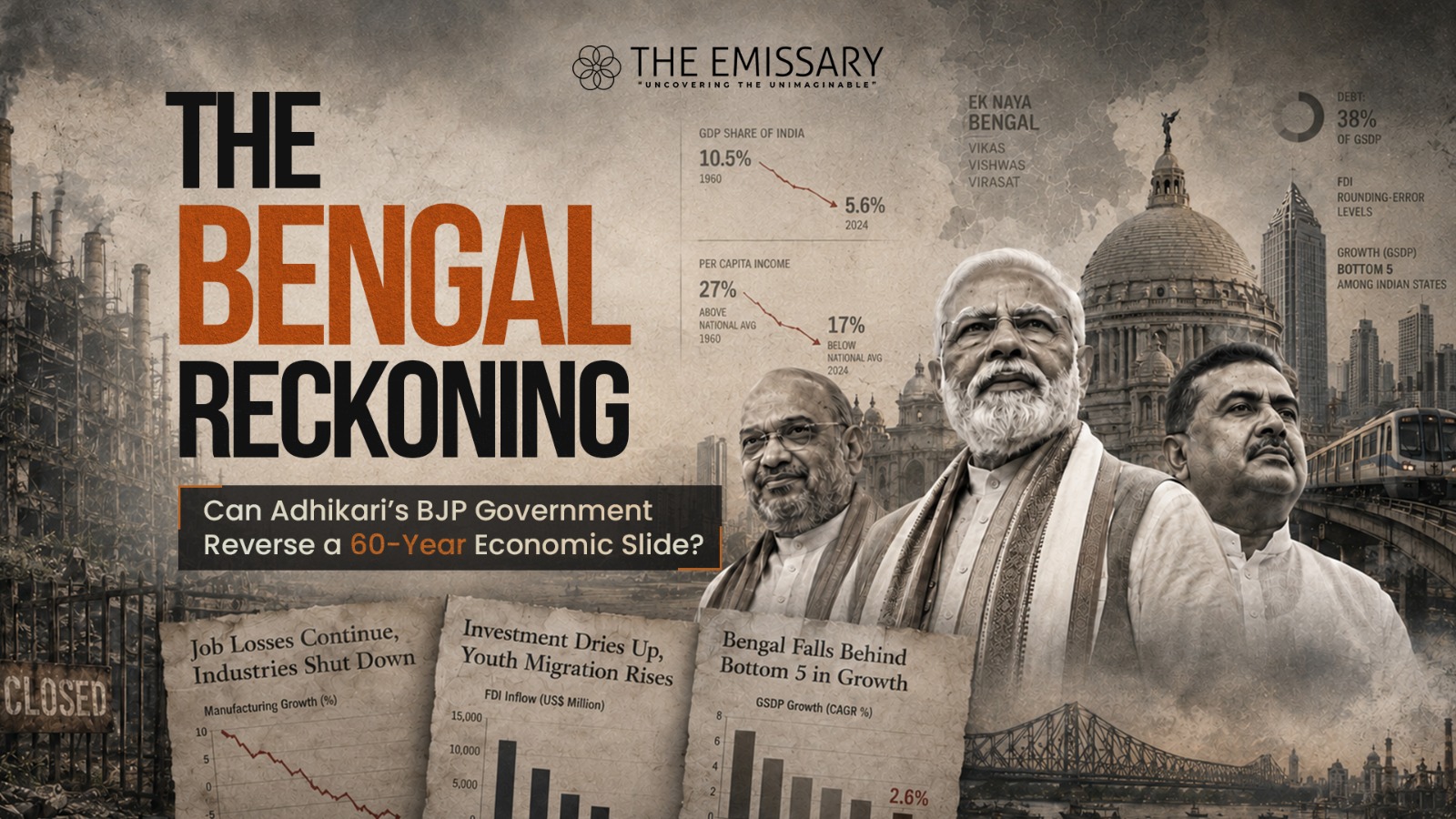

Yet the harder cycle ending with the incoming government is economic, a slide that has lasted six decades, survived three regimes, and quietly turned one of India’s most industrialised states into one of its slowest-growing. The numbers remain stark. West Bengal, which held the third-largest share of national GDP at 10.5 percent in 1960-61, now accounts for only 5.6 percent in 2023-24. West Bengal’s per capita income was above the national average in 1960-61 at 127.5 percent, but its growth has failed to keep pace with national trends. As a result, its relative per capita income declined to 83.7 percent in 2023-24, falling below that of even traditionally laggard states like Rajasthan.

In one human generation, Bengal has gone from earning a quarter more than the average Indian to earning a sixth less. That is the inheritance passed onto the Suvendu-led BJP government.

A six-decade slide, in three movements:

West Bengal’s decline has been remarkably linear, which makes single-cause explanations untenable. It began with the relocation of the national capital from Calcutta to Delhi on February 13, 1931, accelerated through the Freight Equalisation Policy of the 1950s and 1960s, which neutralised Bengal’s mineral-belt advantage by subsidising the transport of coal and steel to coastal manufacturing hubs, and then was institutionalised during the Left Front decades. In recent times, West Bengal’s real GSDP has grown at an average rate of 4.3 percent during the period from 2012-13 to 2021-22 compared to the national average growth of 5.6 percent. Over the longer window from 2013 to 2024, the five slowest-growing states are Meghalaya (3.64%), Goa (4.12%), Puducherry (4.29%), Nagaland (4.55%), and West Bengal (4.59%), placing Bengal in the company of small, structurally constrained economies rather than the large industrial peers it once led.

The Left Front’s role in the state’s economic degradation is well-rehearsed but worth precise framing. The popular narrative often blames militant trade unionism; the statistical record although substantiates other reasons as well. In the year 2003 there were 432 instances of work stoppage. Of them 400 were due to lockouts (employers revoke access of employees to workplace) and only 32 due to strikes, lockouts resulted in a loss of 25,600,000 man days against 1,600,000 from strikes. Over the years 2001-2006 there were 152 strikes and 2,266 lockouts. Bengal’s industrial collapse was driven less by workers withdrawing labour than by capital withdrawing from a state where governance had become unreliable and contracts unenforceable.

The Singur episode of 2006-08 codified that perception globally. The new Sanand factory in Gujarat was completed in just 14 months, compared to the 28 months spent on the Singur facility in West Bengal before Tata, one of India’s largest conglomerates, abandoned the car Nano’s production. The single SMS, “Welcome,” from Narendra Modi as Gujarat Chief Minister to Ratan Tata has become a case study in what it means for a state to lose investor trust. In 2016, an arbitral tribunal mandated ₹765.68 crores from the West Bengal Industrial Development Corporation (WBIDC) to Tata Motors for the losses incurred by the group. The pejorative episode for West Bengal’s industry thurst into prominence Mamata Banerjee’s Trinamool Congress (TMC). The price of Singur was not one factory; it was the chilling signal sent to every large investor evaluating East India for over fifteen years.

The Trinamool years inherited that signal and doubled down on a different model: welfarist redistribution funded by deficit borrowing. The most consequential scheme, Lakshmir Bhandar, gave monthly cash to women voters and was politically successful enough that, in a remarkable irony, BJP had initially opposed the financial model but in its Sankalp Patra or election manifesto, it committed to increase individual benefits under these same schemes or ‘doles’. Once a state organises voters around direct transfers, the gravitational pull is structural, successors must continue or face the same anti-incumbency they exploited.

The fiscal trap:

The harder constraint Adhikari inherits is fiscal. These three states also consistently exceed safe debt-to-GSDP thresholds, Rajasthan at 35.8%, Punjab at 46.6% and West Bengal at 38%. In absolute terms, the state’s total financial debt that stood at ₹1,918 billion (US$20 billion) as of 2011 swelled to ₹3,050 billion (US$32 billion) at the end of 2015-16 and is estimated to further grow to ₹6,932 billion (US$73 billion) at the end of 2024-25. That is a 3.6x increase in the rupee debt stock over fifteen years, financing welfare expansion, salaries, and interest payments rather than capital formation.

On the revenue side, the state is structurally underpowered. The State collects less in own tax and non-tax revenues as compared to a median State. The transfers from the Centre are also lower than that of a median State, but these constitute the largest component of its total revenues. The State’s expenditure-to-GSDP ratio, at 16.5 percent, is lower as compared to a median State due to lower revenue and capital expenditures. The fiscal deficit, at 4.0 percent of GSDP, is higher than that of a median State, as of 2022-23. The revenue deficit, at 2.6 percent of GSDP, in 2022-23 is also higher than a median State’s.West Bengal is, in effect, running deficits a median state would consider imprudent while spending less in productive areas than that same median state.

The credit signal corroborates the diagnosis. West Bengal’s Credit-Deposit Ratio has fallen over the last decade relative to the all-India estimate with a 25 percentage point difference with it as of 2021. The Credit to GSDP Ratio has also declined and deviated further from the India estimate with an 18 percentage point difference as of 2021. Bengalis save in their state’s banks; that money is then lent out elsewhere in the country, because the demand for productive credit, investment, working capital, and expansion, is not present at scale. Foreign capital tells the same story, more bluntly. Maharashtra accounted for the highest share (39%) of total FDI equity inflows in FY 2024-25, followed by Karnataka (13%) and Delhi (12%). Between October 2019-June 2025, FDI inflows in West Bengal stood at Rs. 15,256.66 crore, roughly $1.95 billion over nearly six years, against Maharashtra’s $19.6 billion in a single fiscal. Bengal’s share of national FDI is rounding-error territory. For a state that hosts India’s third-largest metropolitan economy, this is an indictment.

The latent endowment:

And yet, the case for West Bengal, the case any serious investor must run, is not weak. It is sleeping. Start with location. The state sits at the convergence of three of India’s most consequential strategic corridors: the eastern dedicated freight corridor (EDFC) whose terminus is Dankuni; the proposed east-west DFC running to Kharagpur; and the maritime route to ASEAN through the Bay of Bengal. It is the land bridge to the Northeast, the only realistic gateway to Bhutan, Nepal, and northern Bangladesh, and the natural staging post for any India-led “Act East” trade architecture. According to a conservative estimate, the expected cargo at eastern ports would reach around 340 MT by 2030 and around 580 MT by 2040. However, the existing ports on the eastern side face natural restrictions like limited draft, higher maintenance dredging, tidal dependency for vessel transit etc., resulting in capacity constraints. Bengal has the coastline; what it lacks is the draft.

Demography is on its side, barely. Bengal’s working-age population continues to grow even as fertility has fallen below replacement, giving perhaps a fifteen-year window before dependency ratios climb. The MSME base is unusually deep, the state boasts 89 lakh MSME units, employing 1.36 crore people. Among these, 29 lakh units are owned by women entrepreneurs, constituting 32.7% of the total. The agricultural base is formidable, the state is India’s largest rice producer at roughly 13% of national output, second-largest in potatoes and inland fisheries. The Bantala leather complex, almost unknown outside the state, is Asia’s largest. Crucially, industrial growth, however diminished the base, has been quietly outpacing the national average only recently. The industrial sector in West Bengal grew by 7.3% in 2024-25, exceeding the national average of 6.2%. The outgoing West Bengal Government announced that the state has attracted Rs. 1,33,000 crore (US$ 15.38 billion) in private investment and generated 1.8 lakh jobs across sectors such as iron & steel, oil & gas/energy and logistics. The veracity of these claims remain disputed. Nevertheless, it is safe to infer that the bones of an industrial revival exist; what is missing is the connective tissue of land, logistics, and credibility.

What the new government’s manifesto promises and where it falls short?

The BJP’s Sankalp Patra, released by Union Home Minister Amit Shah on 10 April 2026, reads as two documents bolted together. One is a continuation of the welfare state under new branding: Rs 3,000 per month for women under Annapurna Bhandar, Rs 3,000 per month to unemployed people, Rs 3,000 per month for elderly and widowers. Ayusman Bharat, a pan-India health insurance scheme, was launched in the first cabinet meeting of the new government on May 11, 2026, replacing the previous state government’s health insurance scheme Swasthya Sathi. The other is an industrial-modernisation agenda: The BJP manifesto outlines a special, heavily funded development plan to revitalise the Haldia port infrastructure. The state will rapidly develop new deep-sea ports at Tajpur and Kulpi to handle increased international cargo traffic. There are promises on the 7th Pay Commission, 33% reservation in government jobs for women, and on registering fishermen under the Pradhan Mantri Matsya Sampada Yojana to make the state a fish-export hub. On their own, these policy efforts are necessary but not sufficient. Three deeper problems remain largely unaddressed.

First, the land question. Singur did not happen because Tata wanted to evict farmers. It happened because India’s land acquisition framework, even after the 2013 amendment, has no functional path for industrial assembly at scale in densely cultivated, politically organised, multi-crop terrain, which is most of southern Bengal. Building Tajpur, Kulpi, the associated industrial corridors, and the freight links that justify them will require thousands of acres. A government that promises ports without simultaneously announcing a transparent, market-priced, voluntary land-pooling regime with equity participation for landowners on the Magarpatta or Amaravati model is repeating the Buddhadeb Bhattacharjee mistake at greater scale. The manifesto is silent here.

Second, the fiscal arithmetic. The new direct transfers, the 7th Pay Commission, the Ayushman Bharat rollout, and the proposed port and infrastructure capex cannot all be financed simultaneously under a 38% debt-to-GSDP ratio without either central support or revenue-side reform. West Bengal’s own tax revenue at 5.5% in 2025-26, same as the revised estimates for 2024-25 of GSDP is well below the 7-8% achieved by Karnataka or Tamil Nadu. Closing that gap, through stamp duty modernisation, property tax reform in Kolkata and the seven other municipal corporations, GST compliance enforcement, and rationalisation of state excise, would generate the fiscal space that the manifesto’s commitments actually require. No serious revenue agenda has been articulated. Without one, the borrowing path widens.

Third, the credibility problem. This is the hardest, and it is where data give way to political economy. The main reason for the decline is a direct outcome of poor work culture, political interference, and failure of governance that has resulted in industrial anarchy that scares off private investment in the state. Investors do not write cheques to manifestos; they write them to the stickiness of contracts and the predictability of the state. A “white paper on corruption” and a “special judicial commission on political violence,” both promised by the BJP, are useful signalling devices. But what builds credibility is the boring, accumulating evidence of a state government that arbitrates land disputes within fixed timelines, settles GST refunds without discretion, honours power purchase agreements, and prevents localcadre extortion from contractors. None of these can be legislated by ordinance; all of them must be demonstrated, transaction by transaction, over the first eighteen months.

The harder reforms:

If the diagnosis is right, the prescriptions write themselves. Power tariff rationalisation, West Bengal’s industrial power tariff is among India’s highest, partly because the cross-subsidy to agricultural and domestic users is among India’s most aggressive. Bringing it into line with neighbouring Odisha, which has used moderate tariffs to attract aluminium, steel, and chemicals, is a precondition for any port-linked manufacturing strategy. The 0.5% of GSDP fiscal-deficit space the Centre has tied to power-sector reforms is precisely the lever to access.

A Bengal Land Pool Authority modelled on Gujarat’s town planning schemes but adapted to multi-crop agricultural land: voluntary consolidation, market-linked compensation in cash and serviced land, equity stakes for landowners in resulting industrial estates. Without this, Tajpur remains a press release.

Refocusing welfare from cash to capabilities through direct transfers that will continue. But a 10% reallocation from cash schemes to skilling, aligned to garments, electronics assembly, leather, food processing, and gig-economy formalisation, would change Bengal’s labour productivity ceiling. The projected average GSDP growth rate is 7.65 percent for Gujarat, 7.41 percent for Karnataka, and 7.2 percent for Tamil Nadu and 6.16 percent for West Bengal. The 1-1.5 percentage point gap with the top performers is, fundamentally, a productivity gap.

With Bangladesh’s Matarbari deep-sea port operational and northeastern markets growing, Bengal should be the natural beneficiary of aquadrilateral trade architecture spanning Dhaka, Yangon, Kathmandu, and Thimphu. The centre-state alignment now in place creates space for it that did not exist under TMC rule.

Kolkata’s emergence as a knowledge-economy hub. The state’s universities, Jadavpur, IISER Kolkata, produce one of India’s highest densities of STEM graduates per capita, yet IT/BPO share has consistently underperformed Bengaluru and Hyderabad. A targeted GCC policy, tax incentives, single-window approvals, dedicated commercial real estate at New Town and Rajarhat, could capture the next wave of GCC migration that Tier-1 cities are pricing out.

Why a strong Bengal matters to India:

The instinct in Delhi has been to write Bengal off, to treat it as politically interesting but economically marginal in a Maharashtra-Karnataka-Gujarat-Tamil-Nadu growth story. That view is increasingly indefensible. In 2032-33 when India reaches the US$ 7 trillion, the top six states will contribute about half of that. Without Bengal recovering even to its 1990s share, India’s growth becomes more concentrated, more western, more coastal, and the eastern half of the country, including Bihar, Jharkhand, and the Northeast, loses the gravitational anchor it needs.

Beyond aggregates, Bengal is the only large state with simultaneous depth in agriculture, MSME manufacturing, port-linked logistics, and a Tier-1 services metropolis. If India is to rebalance away from over-reliance on western coastal clusters for supply-chain resilience, for strategic reasons in the Bay of Bengal, and for absorbing labour from the Gangetic plain, Bengal is the indispensable piece. The semiconductor partnership with the United States, announced in late 2024, named West Bengal as the proposed location for a nationalsecurity-focused fabrication plant. That bet, made in Wilmington, must now be vindicated in Kolkata.

The Adhikari government will be judged on welfare delivery, communal management, and its handling of an Opposition TMC. But the historical scorecard hinges on something narrower: whether, by 2031, West Bengal’s share of India’s GDP has stopped falling. For sixty years, every government in Kolkata has failed that test. The BJP’s manifesto, generously read, addresses perhaps two-thirds of what the data demands. The remaining third spanning land, fiscal arithmetic, and credibility reforms will determine whether this transition is a political event or an economic one. Bengal has been the inheritance no Indian government wanted. It has now become the inheritance no Indian government can afford to mishandle.