By Leon Barillet

Historical Background

India and China’s trade relationship has transformed from negligible volumes in the mid-20th century to a massive exchange by the 21st century. After the 1962 border war between the two Asian giants, economic ties remained minimal for decades. Diplomatic normalisation in the late 1970s and 1980s slowly reopened commerce, but real growth in trade took off after China’s 2001 entry into the World Trade Organisation. Bilateral trade expanded from only a few billion dollars around 2000 to over $75 billion by 2011. China became India’s largest trading partner by the late 2000s, and trade targets were ambitiously set, a goal to reach $100 billion by 2015. Although that target wasn’t met on schedule, the momentum was undeniable, by 2023, two-way trade hit a record $136 billion. This surge was underpinned by China’s emergence as the “world’s factory” and India’s growing import needs for machinery and electronics, while India exported commodities like iron ore, cotton, and minerals to fuel China’s industrial rise.

This deepening economic engagement unfolded even as strategic relations remained uneasy. Historical mistrust lingers from border conflicts, the background of 1962’s war and standoffs in 1967 and 1987, and more recent clashes such as the Doklam crisis of 2017 and the deadly Galwan Valley skirmish in 2020. Both nations have built up military infrastructure along the Himalayas, and political tensions simmer over issues like China’s ties with Pakistan and India’s hosting of the Tibetan exile community. Yet, throughout these frictions, trade kept climbing. Leaders on both sides often compartmentalised economic ties from strategic disputes, manifested by high-profile summits, like the 2018 Wuhan meeting, aimed at stabilising relations without derailing commerce . This paradox, growing trade interdependence amidst strategic rivalry, has become a defining feature of India-China relations over the past two decades.

Current Trade Landscape

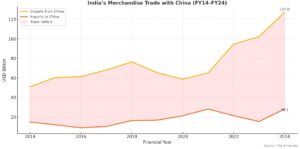

Today, China accounts for an outsized share of India’s trade portfolio, albeit with a severe imbalance. China is second-largest trading partner for India, vying with the United States. In the Indian fiscal year 2023–24, bilateral goods trade reached roughly $118–128 billion, with China supplying the lion’s share. India’s imports from China hit approximately $100–115 billion annually in the most recent year, while its exports to China were only about $15–17 billion. The result is a record trade deficit hovering around $85–100 billion in China’s favour. This gap has widened to unprecedented levels, India’s trade deficit with China for 2024-25 climbed to $99.2 billion, the highest ever. The composition of trade underscores why this imbalance endures, India mainly sells low value-added goods to China such as iron ore, minerals, cotton, and agricultural commodities, while importing vast quantities of high value manufactured products. In 2023, India’s top exports to China included ores, cotton, seafood, and organic chemicals, whereas its imports from China were dominated by electronics, machinery, chemicals, and active pharmaceutical ingredients.

Several policy constraints and barriers shape this trade landscape. India has grown increasingly concerned about over-reliance on Chinese imports and has imposed a range of tariffs and non-tariff barriers in response. Since 2018, New Delhi’s Phased Manufacturing Program and other tariff measures have raised import duties on Chinese electronics, solar panels, toys, and a host of consumer goods to protect domestic industry. India now levies a 40% customs duty on imported solar modules and 25% on solar cells, a move aimed squarely at Chinese suppliers who until recently dominated India’s solar installations. Similarly, basic import duty on toys was tripled from 20% to 60%, coupled with stringent quality control orders, to curb inexpensive Chinese toys flooding the market. These steps reflect motivations both economic, shielding local manufacturers from dumping and unfairly cheap imports, and strategic, reducing exposure in sensitive sectors. Indian regulators have also banned hundreds of Chinese mobile apps, including popular ones like TikTok and WeChat, citing national security and data privacy concerns following the lethal 2020 border clash. Inward investment from China faces tighter scrutiny as well. In April 2020, India revised its foreign investment rules to require government approval for any investment originating from countries sharing a land border, a de facto restriction on Chinese capital. This policy, instituted amid fears of opportunistic takeovers during the pandemic, dramatically slowed Chinese FDI into India. Therefore, by 2021, Chinese FDI inflows had plummeted to about $280 million from over $500 million in 2019.

China, for its part, maintains market access barriers in areas where India is competitive. Indian officials note that Beijing has been slow to open its markets to Indian pharmaceuticals and agricultural products, using regulatory hurdles to limit imports of Indian generic drugs, dairy, meat, and other goods. Indian IT services, a world-leading sector, also have scant presence in China’s market due to opaque regulations and China’s preference for domestic tech firms. These barriers mean India’s export basket to China remains narrowly based on raw materials. Meanwhile, China’s exports face comparatively fewer hurdles entering India aside from India’s recent protective measures. The net effect is a trading relationship where Beijing enjoys a broad surplus and New Delhi frets about dependency. It is telling that China alone accounts for about 15% of India’s total merchandise imports by value, a startling figure given that this excludes oil, India’s biggest import, sourced mostly from elsewhere. In categories like electronics, China’s share of India’s imports is routinely 40–45%, and for machinery around 35–40%. Such dominance has raised alarms in New Delhi that economic leverage could translate to strategic vulnerability in times of crisis. Unsurprisingly, current trade policies on both sides are increasingly coloured by national security calculations and geopolitical motives, not just pure market logic.

Sector-Specific Strategic Vulnerabilities

India’s vulnerable sectors, a few critical sectors illustrate India’s strategic susceptibility due to heavy dependence on Chinese imports and limited alternative sources.

1. Electronics and Telecom: India’s electronics supply chain is deeply entwined with China. An estimated 40–45% of India’s electronics, telecom equipment, and electrical machinery imports come from China. Chinese-made smartphones, network gear, computer hardware and components have long dominated Indian markets because of their cost competitiveness. Even as India assembles phones domestically, most core components such as chips, displays, and batteries are sourced from China or Chinese firms elsewhere. If Beijing were to restrict exports of semiconductors, phone components or telecom gear, Indian consumers and businesses would face disruptions. Domestic production capacity for advanced electronics remains nascent, so replacement options are limited in the short term. A study by the Indian Institute of Foreign Trade found China was the cheapest or sole supplier for dozens of electronics sub-categories critical to Indian industry. This makes quick diversification challenging, Chinese inputs are often the only economically viable choice for Indian manufacturers.

2. Pharmaceutical APIs: India is a global pharmaceutical powerhouse in finished generic drugs, but it relies overwhelmingly on China for the Active Pharmaceutical Ingredients (API) and bulk drugs needed to make those medicines. Between 70% to as much as 100% of the supply of certain critical APIs for Indian pharma comes from China. This includes key antibiotic ingredients, painkiller chemicals, and vitamin components. In an alarming episode during the COVID-19 pandemic, China temporarily halted exports of some APIs, which forced India to curtail its own medicine exports until supplies stabilised. In strategic terms, Beijing holds a chokehold, a deliberate Chinese export ban of pharmaceutical ingredients would leave India scrambling for expensive alternatives or importing ready-made drugs at higher cost. Building local API manufacturing will take years, so this dependency remains a major strategic liability in the interim.

3. Renewable Energy Technology (particularly solar): India’s ambitious solar power program is underpinned by Chinese hardware. Roughly 70% or more of India’s solar modules and cells have been of Chinese origin, given China’s dominance in the global photovoltaic supply chain. Recent tariffs have reduced the direct share of Chinese imports, China supplied about 62.6% of India’s solar equipment imports in FY2023-24, down from over 90% a few years prior, but Chinese manufacturers still effectively control the market via lower-cost products. Moreover, China produces 97% of the world’s solar-grade polysilicon and the vast majority of solar wafers. India currently has negligible capacity in those upstream inputs, making it dependent on either Chinese imports or Chinese-owned suppliers in third countries. Should China curtail exports or dramatically raise prices, India’s renewable energy plans, 500 GW of renewables by 2030, with solar as a pillar, could be derailed. This is a strategic concern as clean energy is linked to both economic security and climate goals.

4. Automotive and EV Components: A newer vulnerability is emerging in electric vehicles and advanced automotive components. China holds a near-monopoly in certain rare earth materials and magnets used for EV motors and wind turbines. In 2025, China imposed export licensing controls on rare earth magnets and related inputs, causing Indian EV manufacturers serious concern. India currently relies on China for 93% of the rare earth magnets it uses in EV motors. If bureaucratic delays or export denials from China persist, reports indicate new Chinese rules can delay shipments by 45 days or more, Indian companies could face production halts within weeks due to lack of key materials. The broader automotive sector in India also sources many electronic parts, sensors, and battery cells from China. With transportation electrification being a strategic priority for India, this dependency on Chinese technology, from lithium-ion cells to power electronics, represents a strategic weak point that China could exploit or that could become a casualty if relations worsen.

5. Industrial Machinery and Chemicals: China is the world’s top supplier of industrial machines, factory equipment, and many chemicals, and India is a major buyer. Nearly 40% of India’s machinery imports, from heavy machinery to textile machines, come from China. Additionally, China supplies over a quarter of India’s imported chemicals and pharmaceutical inputs. Many Indian factories, from textiles to plastics, cannot easily source specialised machinery or certain chemical feedstocks from elsewhere at comparable cost and scale. This creates a structural reliance. In a contingency where Chinese machinery or chemical exports were cut off, Indian manufacturing across sectors would feel the strain, impacting everything from infrastructure projects, which use Chinese-made tunnelling and power equipment, to small manufacturers reliant on Chinese chemicals.

Collectively, these examples underscore an uncomfortable reality for India, its fastest-growing and strategically significant industries often depend on Chinese inputs. Attempts to find alternate suppliers reveal that often only a handful of global players exist, and Chinese firms are frequently the most competitive or have spare capacity. While Japan, South Korea, Europe, or domestic sources can substitute in some areas, it would take considerable time and cost for them to fill the gap left by China in many supply chains. This imbalance leaves India potentially exposed to economic coercion. Beijing could impose painful costs on India by weaponising trade, as seems to be the trend since the election of the new U.S. administration, whereas India has limited ability to retaliate in kind given the asymmetric flows.

In contrast, China’s strategic dependence on Indian exports is minimal, a reflection of the skewed trade structure. India’s exports to China are mostly commodities and raw materials that, while useful to Chinese industry, can be sourced from other countries if needed. India has supplied iron ore to China’s steel industry, especially in the 2000s, but China could ramp up imports from Australia or Brazil if Indian ore became unavailable. India is also a major exporter of cotton, including to Chinese textile mills, but again China could turn to the US, Brazil, or its own polyester production if pressed. Agricultural products like Indian rice and seafood, such as shrimp, have a growing market in China, in 2023, crustaceans and fish meal were significant Indian exports, yet these too are replaceable by other global suppliers or domestic Chinese output.

One area where China does import a high volume from India is certain minerals and ores, India’s exports of ores, slag, and ash to China were over $3 billion in 2023. But even here, alternate sources, Australia, Indonesia, and African nations mean Beijing is not uniquely beholden to New Delhi. Unlike the high-tech or specialised nature of India’s imports, China mostly buys generic commodities from India. Should India cut off these exports as a punitive measure, it might hurt specific Chinese companies in the short run but would be unlikely to cripple any strategic Chinese industry. China’s biggest potential vulnerability is not a specific commodity from India, but the loss of the Indian market itself. India’s 1.4 billion population and its growing consumer market are important for Chinese firms’ growth. Chinese smartphone makers, appliance brands, and infrastructure companies have prospered in India, until recent restrictions. If India’s market is partly closed to China, as is happening in sectors like telecom and tech, it does pinch Chinese business interests. But from Beijing’s strategic perspective, this is a tolerable cost given China’s diversified export destinations. In sum, the interdependence is greatly lopsided, India needs Chinese goods far more than China needs any specific Indian goods. This asymmetry is at the core of India’s strategic dilemma in managing trade with China.

India’s Response to Strategic Trade Pressures

Aware of these vulnerabilities, India has undertaken a multi-pronged strategy to insulate its economy from perceived Chinese predatory trade practices, dumping, and over-reliance. Key elements of New Delhi’s response include, protective tariffs and duties as India has significantly raised import tariffs on a range of Chinese products over the past five years to encourage domestic substitution. Electronics and electrical goods, a category where Chinese imports are dominant, have seen successive duty hikes. The government increased customs duties on mobile phones and components, televisions, and other appliances, explicitly aiming to make imports costlier and spur local manufacturing. In renewable energy, as noted, a 40% duty on solar modules was introduced in 2022 to cut dependence on cheap Chinese solar imports. Similar heavy tariffs were placed on toy imports, raised to 60%, to stem the flow of inexpensive Chinese toys. These tariff walls, while raising consumer prices marginally, have shown results, toy imports, dropped by over 70% between 2018–19 and 2023–24 after the higher duties and quality controls came into force. Overall, India’s average tariff on Chinese goods has risen, indicating a deliberate move to use trade policy as an economic defense tool.

Anti-Dumping Investigations and Quality Control are another step pursued by India more aggressively in deploying anti-dumping and technical standards to check Chinese imports. Dozens of anti-dumping investigations have been launched or revived targeting Chinese products ranging from steel and chemicals to electronics and pharmaceuticals. In fact, by 2021 India had resumed or initiated 220 out of 370 anti-dumping cases against China, many of which had languished, to penalise under-priced imports. These duties act as tariffs on specific items found to be dumped at unfair prices. Withal, India has tightened quality and safety standards to filter imports. The Bureau of Indian Standards (BIS) introduced strict certification requirements for products like toys, electronics, and even solar equipment. Since January 2021, all toys sold in India must meet BIS safety norms, a rule that effectively shut out many unregulated Chinese toy imports that failed to comply. Similar standards are being extended to electronics and machinery, forcing importers to ensure products meet Indian certifications. While couched as consumer safety measures, these serve the dual purpose of raising the bar (and cost) for foreign imports, disproportionately affecting Chinese suppliers who previously competed heavily on price while sometimes skimping on quality.

Post-Galwan 2020, India moved swiftly to restrict Chinese presence in critical sectors. Besides the aforementioned FDI approval rule for neighbours, which essentially froze most new Chinese investments in Indian startups and infrastructure projects, the government barred Chinese companies from sensitive public procurement. Chinese firms are no longer allowed to bid for contracts in telecom infrastructure, railways, power equipment for the national grid, and other strategic areas without special permission, a measure justified on security grounds. In telecom, India has effectively excluded China’s Huawei and ZTE from its 5G rollout, aligning with partners like the U.S. and Australia in viewing Chinese telecom gear as a potential espionage threat. Regulations now mandate telecom operators to purchase equipment from “trusted sources” and avoid vendors from adversary nations, which in practice blocks Chinese 5G hardware. India also banned over 300 Chinese mobile apps between 2020 and 2022, citing data security, a sweeping digital decoupling that cut off Chinese tech firms from accessing Indian user data and advertising markets. These steps represent a security-first approach to economic links, if a Chinese product or investment is seen as a potential tool of influence or intelligence, it is swiftly curtailed, even at the cost of economic efficiency.

More on the inward offensive side, India has launched Production-Linked Incentive (PLI) schemes in over a dozen sectors to boost domestic manufacturing and substitute imports. With nearly $26 billion in incentive outlays , PLI programs offer companies subsidies and support to make everything from electronics to pharmaceuticals in India. The explicit goal is twofold, increase manufacturing’s share of GDP and reduce reliance on China in key sectors. The electronics PLI, for instance, has lured global players like Apple’s contract manufacturers into setting up large smartphone assembly units in India. As a result, India’s electronics exports have climbed, Apple now produces about 20% of its iPhones in India, and imports of finished devices from China have moderated. However, as a Hinrich Foundation analysis points out, while downstream assembly has grown, India still imports upstream components from China in many cases. In pharmaceuticals, a PLI for bulk drugs and APIs aims to resurrect domestic production of molecules where China currently dominates. Dozens of new API plants are being set up with government support, targeting molecules where India was nearly 100% import-dependent. Early signs show a small reduction in China’s share of India’s API imports, from ~75% to 72% in recent years, progress, albeit modest, toward delinking vital pharma supply chains. Similarly, PLIs in solar equipment are pushing domestic panel manufacturing, and in advanced batteries to reduce EV component imports. India is essentially using industrial policy as a strategic buffer, incentivising companies to Make in India what they used to import from China.

The Indian government is also improving its monitoring of import surges and trade circumvention. Officials have set up a dedicated “monitoring cell” to track imports, especially cheap goods potentially rerouted through third countries to bypass direct Chinese origin labelling. This was partly in response to anecdotal evidence that some Chinese products, like electronics or chemicals, were coming via ASEAN nations or Hong Kong to exploit free trade agreements or obscure their source. Customs authorities have been tightening rules-of-origin scrutiny to ensure Chinese goods don’t enter unfairly under the cover of another country’s trade pact. India has even warned domestic companies against helping Chinese firms dodge U.S. tariffs by re-exporting to America through India. Enforcement of trade remedies has likewise been strengthened, with faster investigations into dumping complaints and more proactive use of safeguard measures if a sudden import spike threatens a local industry. The subtext is clear, New Delhi is far more alert to trade asymmetries now and willing to act decisively, whereas in the past a laissez-faire approach often prevailed in the name of free trade.

Through these measures, India is trying to strike a balance, shielding critical sectors and motivating domestic producers, without resorting to an overt trade war. The results so far are mixed. Imports from China have continued to grow despite higher barriers, China’s share of Indian imports even increased over the last 15 years in industrial goods, suggesting India’s demand still outstrips what domestic alternatives can fulfil. However, there are pockets of success as mentioned previously, certain industries like toys and mobile phone assembly are less dominated by China than before, thanks to targeted policies. The government’s challenge is to emulate these successes across more sectors without unduly raising costs. Each policy response, tariff or ban, comes with the risk of unintended fallout, higher input costs for industry or retaliatory actions by China. Thus far, Beijing’s official response to India’s curbs has been muted, perhaps because Chinese exports overall remain robust. But India’s resolve in countering perceived unfair trade practices is clearly hardened, reflecting a broader shift toward economic self-reliance (Atmanirbhar Bharat) driven by strategic imperatives.

Economic Outlook and Future Trade Trajectory

Looking ahead, the trajectory of India-China trade will be shaped by the two countries’ diverging economic paths and priorities. Growth projections designate India to expand faster in percentage terms, while China’s growth moderates as its economy matures. The International Monetary Fund expects India to grow around 6% in 2024–25, outpacing China’s projected 4–5% growth. Over the next decade, India, now the world’s fourth-largest economy, is forecast to become the third-largest, overtaking Germany, while China will remain firmly the second-largest, behind only the U.S.. In the year, India’s GDP would surpass $5 trillion or more, still only a fraction of China’s, but with a much younger population and rising consumption. This means India’s import needs will likely increase as its economy and middle class grow, potentially expanding the market for Chinese goods further. Unless India’s industrial base catches up, it may continue to rely on China for affordable capital goods and consumer products to fuel its growth. Indeed, the current trend shows that even in years when India’s overall imports decline, due to global factors, imports from China often keep rising, indicating a structural dependence.

However, India’s economic priorities could alter the composition of this trade. New Delhi is determined to boost domestic manufacturing and high-tech industries, from electronics to defense to electric vehicles. If these initiatives bear fruit, India might produce more at home or source from a broader array of partners, thereby tempering the growth of Chinese imports. Should India succeed in developing its own semiconductor assembly facilities with help from allies, future imports of Chinese chips might decrease. Or if Indian firms capture a larger share of the solar panel value chain, the reliance on Chinese solar equipment may plateau and then fall. In essence, India is aiming for a scenario where it can grow rapidly without its import bill from China ballooning in tandem, a decoupling of growth from Chinese dependency. This will require overcoming significant hurdles, regulatory bottlenecks, skill gaps, higher production costs in India, and an entrenched Chinese supply chain that is hard to beat on efficiency.

China’s economic trajectory, meanwhile, is tilting toward higher-value industries and selfsufficiency in technology. Beijing’s focus in the coming years is on indigenous innovation in semiconductors, aerospace, and advanced manufacturing, while reducing its own dependence on imports of things like chips or Western software. This shift could mean China will be exporting more high-tech capital goods, areas where India either might not import due to security concerns or might not yet have demand. Conversely, as Chinese wages rise and its low-end manufacturing relocates to cheaper countries, India might import those low-end goods from alternate sources like Vietnam or Bangladesh instead of China. In theory, this could slow the growth of bilateral trade or even shrink it in some sectors. In practice, however, Chinese companies are adept at moving production within their ecosystem, many have set up plants in Southeast Asia that send goods to India, effectively maintaining China’s supply chain influence in another form. Unless India joins trade agreements or builds equivalent supply chains, Chinese-linked products will find their way to its shores one way or another.

One notable dynamic will be competition in third markets. As India ramps up its own manufacturing, say in smartphones or pharmaceuticals, it could start competing with Chinese exports in regions like Africa, the Middle East, and South Asia. This could introduce a geopoliticaleconomic competition, both countries vying to export similar goods to the developing world. We see early signs in areas like mobile phones, where Indian assembly for brands like Apple is turning India into an export base, potentially grabbing market share that might have belonged to Chinese exports. Similarly, India’s emergence as a low-cost car exporter, especially for gasoline cars now, and possibly EVs later, could compete with Chinese automakers in some markets. If India’s export prowess grows, it might partially offset its China import dependence by earning foreign exchange from exports in those same product categories. After all, China owns the title of the “factory of the world.” The two nations could have a more balanced trade relationship not by trading a lot more with each other, but by each trading with the rest of the world, India supplying where China currently does, and thereby reducing its need to buy from China.

Politically, the strategic trust deficit between India and China is likely to persist, which places a ceiling on how much the trade relationship can deepen in a healthy way. Major breakthroughs, such as a free trade agreement or large-scale Chinese infrastructure investments in India, appear highly unlikely under present circumstances. Instead, the economic ties will be managed through a wary lens. India will continue scrutinising Chinese investments and imports for security implications, while China will remain cautious about India’s closer alignment with Western economies. This could result in a gradual decoupling in sensitive domains in tech, defense, and telecommunications, even as less sensitive trade (commodities, basic consumer goods) carries on robustly. In numeric terms, bilateral trade may continue setting new records in the short term, given sheer demand and lack of alternatives, but its character will change, more bargaining, more safeguards, and slower growth relative to each country’s overall trade expansion. Already, in 2023, growth in India-China trade slowed to about 1.5%, much lower than previous years, hinting at a plateauing trend. Some data even show a slight dip in 2023 imports from China compared to 2022, possibly due to India’s diversification efforts.

Over the long run, if India’s economy continues to grow fast and its industrial policies succeed, we could see a scenario where India narrows the gap, not eliminating the trade deficit, given China’s head-start and scale but reducing it to more manageable levels. India’s trade with the U.S. already surpassed China in recent years, with India running a surplus with the U.S., demonstrating that India can cultivate other major partners. Trading blocs such as the European Union (EU) and the Gulf Cooperation Council (GCC) trump both the U.S. and China in trade volume with India. Should India replicate that model with the EU, Japan, ASEAN and others, China’s share of India’s import pie might shrink to a less strategically concerning level. Nonetheless, for the foreseeable future, China will remain a crucial, if complicated, economic partner for India. The two Asian giants’ growth stories are interlinked, each supplies what the other needs, cheap goods in one direction, raw materials and a big market in the other. How they manage this interdependency amid strategic distrust will be a defining factor in Asia’s economic landscape. The likely trajectory is continued trade with cautious diversification: India won’t sever trade ties with China, the economic cost would be too great, but it will certainly seek to prune the risks and excessive dependencies within that trade.

Strategic Balancing by Sector

To navigate the fine line between minimising risk and preserving economic benefits, India must practice strategic balancing on a sector-by-sector basis. Not all imports from China are equally critical, and not all can or should be eliminated. Here’s how India can calibrate its approach across sectors. Primarily, India must identify and prioritise critical sectors for de-risking, the first step is to clearly delineate which imports constitute a strategic vulnerability. Heavy industrial machinery, electronics and semiconductors, pharmaceuticals, APIs and medical devices, telecommunications gear, power infrastructure, and solar energy equipment stand out as sectors where dependency on China carries national security or high economic risks. In these sectors, India should put its main focus on risk reduction. That means ramping up domestic capacity, through incentives, R&D support, and skilling programs, and diversifying import sources. For pharmaceuticals, India can intensify joint ventures with Japanese and European firms to produce essential APIs locally; for telecom and 5G, source more from trusted suppliers in Scandinavia or South Korea; for rare earths and battery materials, partner with Australia and Japan to develop alternate supply chains. Not every component can be home-made economically, but even shifting a portion of sourcing away from China or keeping strategic stockpiles could reduce vulnerability. The goal in these critical sectors is to ensure that if tomorrow trade with China was disrupted, India’s economy would not grind to a halt. Recent moves like inviting global semiconductor firms to invest in India, or collaborating with the U.S. on securing critical minerals, reflect this prioritised de-coupling in high-risk arenas.

Secondly, maintaining engagement in non-critical, consumer-driven sectors, where imports from China do not pose a direct strategic threat, often low-end consumer goods, textiles, household items, India can afford to maintain trade relatively untouched, while gradually encouraging local alternatives. Importing Chinese toys or cheap apparel doesn’t endanger national security, though it can impact domestic producers. India has still acted to foster its toy industry, with tariffs and standards, but this was as much about quality and supporting cottage industries as about strategic concerns. Where Chinese imports simply help keep consumer prices low, inexpensive electronics accessories, furniture, and home appliances, India might cautiously continue these imports to benefit consumers and prevent inflation, even as it works to bolster domestic competition. The idea is not to cut off every import, but to weigh the cost-benefit, if an import dependency doesn’t give China undue leverage and fills an important gap affordably, it can be tolerated until viable alternatives emerge. Many Indian small businesses actually rely on imports of Chinese inputs like, cheap motors or fabrics, to then produce finished goods. Shutting these off abruptly could harm Indian livelihoods more than Chinese exporters. Thus, a calibrated approach would keep trade flowing in such sectors but monitor for unfair trade practices. If dumping is detected, selling below cost to kill local industry, then anti-dumping duties should be applied, otherwise, open trade can continue.

Even when India must import, it can try to ensure it isn’t sourcing solely from China. Take electronics, if currently 70% of a particular component comes from China, India could aim to bring that down by developing alternate suppliers, whether domestic or in other countries. Government and industry bodies can facilitate matchmaking with non-Chinese suppliers and offer importers incentives or credit support to buy from elsewhere even if it’s slightly more expensive. Over time, this creates a more resilient supply chain. For critical minerals and rare earths, India has entered into agreements with Australia and Kazakhstan to source lithium, cobalt, and rare earth supplies, anticipating the need to counter China’s dominance. In pharmaceuticals, India is exploring sourcing APIs from countries like Italy or the U.S. for certain drugs, despite higher costs, just to have second suppliers. The principle is akin to not putting all eggs in one basket. Even if China remains the largest supplier in many areas, India can reduce the risk of a single point of failure by nurturing multiple supply lines.

There are sectors where engagement with China could actually be beneficial for India if managed wisely, and thus should not be outright shunned. Renewable energy is one example, India needs vast amounts of solar and battery tech to meet its climate goals, and Chinese firms are the global leaders in scaling these at low cost. Strategic balancing here means continuing to import what is needed to accelerate India’s green transition, it’s in India’s interest to deploy solar quickly, which Chinese supply facilitates, but simultaneously demanding technology transfers or setting up joint ventures to localise production over time. If Chinese companies want to access India’s huge market, India can negotiate terms that build its long-term capabilities. We see hints of this with recent talks, India is considering allowing major Chinese electric vehicle battery makers and solar manufacturers to invest in India under joint venture models, so that production happens on Indian soil, with Indian partners and labor, rather than simply importing finished products. This kind of engagement, conditional and monitored, could turn a dependency into an opportunity for capacity-building. That said, India will need strong oversight to ensure any such partnerships don’t compromise security.

As deliberated often among policy circles, India could institutionalise this balancing act by creating a high-level team that continuously evaluates each sector’s exposure to China. This team, cutting across ministries including commerce, industry, defense, and IT, would craft strategies tailored to each sector. For semiconductors, it might push U.S. partnerships and domestic fabs; for pharma, a mix of PLIs and sourcing from allies; for textiles, where China supplies machinery and synthetic yarn, maybe focus on importing from friendly nations like South Korea or Indonesia. Each sector plan would detail immediate mitigation, alternate suppliers, stockpiles and long-term indigenisation. The government has started moving in this direction with initiatives like the China Cell in the commerce ministry that was reportedly set up to coordinate responses on trade issues. Making this a permanent, empowered body would help avoid ad-hoc decisions and ensure a coherent balancing strategy that is regularly updated as industries evolve.

India’s aim should be to selectively decouple in the most sensitive areas while sustaining mutually beneficial trade elsewhere. It is neither feasible nor necessary to cut economic ties wholesale; the costs to India’s growth and consumer welfare would be too high. Instead, India can build shock absorbers into the relationship: maintain trade volumes but with less fragility. Over time, as India strengthens itself in key sectors, through joint ventures, innovation, and diversification, the nature of India-China trade could shift from one of dependency to one of more equal footing, where India trades by choice, not compulsion. Until then, meticulous sector-wise management is India’s best bet to mitigate strategic risks without sacrificing the economic gains of globalisation.

US-China Rivalry Influence

The intensifying strategic contest between the United States and China serves as a powerful undercurrent in India-China trade dynamics. In many ways, U.S.-China rivalry amplifies India’s dilemmas and opportunities.

On one hand, the U.S.-China trade war and tech war have caused supply chain ripples that directly affect India. As Washington slapped tariffs on Chinese goods and restricted Chinese tech, such as banning exports of advanced semiconductors to China, Chinese firms have sought to redirect their products to other markets. India, as a large growing market not aligned with the U.S. sanctions, becomes an attractive destination for this overflow. When the U.S. hiked tariffs on Chinese electronics, there were fears that Chinese suppliers would dump excess inventory into India or offer cut-rate deals to Indian importers. In early 2025, Indian officials noted a surge in imports of electronics, batteries, and solar cells, partly attributed to Chinese exporters finding alternative outlets amid U.S. restrictions. This “trade diversion” can widen India’s deficit and hurt domestic players if not checked. It prompted New Delhi to enhance its monitoring as mentioned before, setting up cells to track sudden inflows, and to warn Indian companies against becoming conduits for Chinese goods that can’t enter Western markets. Thus, U.S. pressure on China can indirectly flood India with Chinese goods, requiring India to be vigilant to avoid being a dumping ground.

Conversely, the U.S.-China rivalry has opened strategic space for India to reposition itself. The U.S. and its allies now see India as a crucial partner in building resilient supply chains outside of China. Washington has explicitly encouraged a “China+1” strategy to its companies, meaning keep China as a sourcing base but develop another hub like India or Vietnam to hedge bets. India’s large workforce and improving business climate make it a prime candidate. We are seeing tangible results, global giants from Apple to Samsung to Cisco have expanded manufacturing in India as part of diversifying away from China, often with tacit or explicit backing from Western governments. The Quad grouping of India, United States, Japan, and Australia has a working group on supply chain security that focuses on critical areas like semiconductors and rare earths. The United States has also long exhibited willingness to assist India in identifying alternatives for Chinese imports. American officials have floated ideas like a dedicated trade initiative for tech with India, or even a limited free trade agreement in key sectors, to facilitate this shift. In essence, U.S.-China rivalry has made India more geopolitically valuable, which New Delhi can leverage to get investment, technology and market access that help it reduce dependence on China. As one analysis noted, if Washington wants India to counterbalance China, it’s in U.S. interests to bolster India’s economic strength and “de-risking” efforts.

Another impact is in the technology domain. U.S. sanctions have cut off China’s access to certain advanced chips and equipment. India, aligning with the U.S. on strategic tech standards, has kept Chinese 5G and telecom equipment out, and is collaborating with the U.S. on emerging tech, through initiatives like the Indo-U.S. Critical and Emerging Technology iCET partnership. This alignment means India will likely adopt Western tech ecosystems, 5G infrastructure from European vendors, and cloud services from American firms over Chinese alternatives. In the short term, that reduces some imports from China, India essentially imported zero Huawei/ZTE 5G gear, opting for Nokia, Ericsson, etc. In the long run, it binds India closer to Western supply chains, reinforcing a partial economic decoupling from China in high-tech sectors. However, it also means India must navigate Chinese retaliation carefully. Beijing has shown a propensity to retaliate economically against countries aligning with U.S. positions, as seen with its trade curbs on Australian commodities when Australia pushed for a COVID origin inquiry. If India tilts too far towards the U.S., China could target India’s interests, perhaps via stricter customs on Indian goods, or by courting neighbours like Pakistan with trade perks to isolate India. Something we are already seeing. So far, China’s response to India’s U.S. lean has been more along political lines, berating the Quad as a containment tool, than direct trade punishment, likely because China still profits greatly from trading with India.

The U.S.-China rivalry also manifests in the Indo-Pacific strategy, where India is a linchpin of the “free and open Indo-Pacific” vision. There is concern in Washington that if China can pressure India economically, India might hesitate to fully support U.S.-led initiatives against China. If India were overly reliant on China for say, pharmaceuticals or critical electronics, Beijing’s threat to cut those off could deter India from siding with the U.S. on a contentious issue like sanctioning China or conducting naval exercises in the South China Sea. U.S. policymakers are aware of this and thus eager to immunise India from Chinese leverage by deepening U.S.-India trade and tech ties. Indubitably, the second Trump administration has imbued uncertainty in these efforts as well. Recent moves, such as the U.S. inviting India into its semiconductor supply chain cooperation and the signing of an agreement for the U.S. to support India’s semiconductor initiative with expertise, aim to fill gaps that China could exploit. Additionally, after Russia’s Ukraine invasion, India started settling some oil trade in Chinese yuan, something the Indian government is uneasy about. The U.S.-China financial rivalry, with the yuan’s role potentially growing, might put India in a tough spot regarding currency dependence if, more of its trade is invoiced in yuan. So far that’s limited, but it’s another front where big power rivalry could trickle into India-China trade, such as western sanctions pushing India to use yuan for Russian oil, inadvertently increasing India’s yuan exposure, which the U.S. would not favour.

Finally, the U.S.-China rift has spurred multilateral groupings and frameworks that influence IndiaChina trade indirectly. India has joined forums like the Indo-Pacific Economic Framework (IPEF) and is strengthening ties with ASEAN, presumably to integrate more with economies other than China. Meanwhile, China is shoring up RCEP and BRICS as counterweights. This could lead to a bifurcation in trade networks, with India gravitating to one set and China to another, again shaping trade flows. If IPEF leads to common standards or easier supply chain movement among members, which include India, Japan, Australia, etc., then Indian importers might prefer sourcing within that bloc rather than from China. Likewise, China’s push for its own digital payment systems, logistics corridors, and trade rules might exclude India. In the long run, a partial economic deglobalisation along geopolitical lines is possible, where trade blocs mirror security blocs. India’s challenge will be extracting gains from both sides without being forced into a strict camp. So far, India has adroitly sustained a non-aligned stance, banning Chinese tech while still buying record amounts of Chinese goods, and participating in the Quad while also in the BRICS. But if U.S.-China tensions sharpen further, this balancing will be tested. We might see more explicit linkages between strategic stance and trade, the U.S. offering India better market access if it distances from China, or China offering concessions, opening its markets a bit more to Indian goods or restoring border calm, if India softens Quad activities. How India calibrates its choices in this great-power rivalry will directly impact the volume and nature of its trade with China.

Alternative Partnerships and Domestic Capability

In response to both the challenges and opportunities discussed, India is actively forging alternative trade partnerships and investing in domestic capabilities to diversify its economic dependencies. This twin strategy of “friend-shoring” externally and “self-reliance” internally, is central to India’s economic statecraft in the face of China’s rise.

India has accelerated efforts to deepen trade and investment ties with a range of partners beyond China. In the past couple of years, India sealed new trade agreements with like-minded economies, a Comprehensive Economic Partnership Agreement (CEPA) with the UAE in 2022, an Economic Cooperation and Trade Agreement (ECTA) with Australia in 2022, a Free Trade Agreement (FTA) with the European Free Trade Association (EFTA, including Switzerland, Lichtenstein, Iceland and Norway) and recently concluded with the UK. The EU and India, during the visit of EU college of commissioners in January 2025, agreed to conclude a FTA by the end of the year. It is imperative to keep in mind that an FTA does not by itself turbocharge trade among signing parties, yet it is a reliable parameter of global trade integration. These agreements aim to boost exports and secure critical imports from more trusted sources. The India-Australia pact not only lowers tariffs but also opens avenues for collaboration in minerals and education, giving India a friendlier source for commodities like coal and lithium, and reducing reliance on China for those. The Quad alliance is not a trade bloc, but it has facilitated initiatives like the Quad Supply Chain Resilience Initiative. Under this, the three Pacific partners have been sharing information and coordinating with India to identify weak links in supply chains, like semiconductors, and medical supplies, to invest in alternatives. Japan, has invested in infrastructure projects in India’s Northeast, partly to spur industry there and provide an alternative to Chinese infrastructure financing in South Asia. Japan and India have also announced a partnership on clean energy supply chains, covering areas such as hydrogen technology and battery storage, which could wean India off Chinese solar batteries over time.

India is also leveraging its leadership in forums like the G20 and “Global South” diplomacy to craft economic coalitions. During its G20 presidency in 2023, India championed resilient supply chains and even mooted an initiative for trusted supply networks among democratic nations. With ASEAN, India has a long-standing FTA and is now working on upgrading it to cover newer areas like services and digital trade, again with an eye to tightening links with Southeast Asia as an alternative manufacturing source. Notably, countries like Vietnam, Thailand, and Indonesia have gained Indian market share in categories once dominated by China, a trend India encourages, as imports from those countries are seen as less strategically worrying, and often those nations are also wary of China. India is pushing to integrate with global value chains led by the U.S., EU, and East Asian economies so that it can import intermediate goods from a diversified set of countries and export finished goods worldwide. This diversification doesn’t mean India will import zero from China, but if a particular item can be sourced from, say, South Korea or France competitively, India is keen to do so even if China offers a slightly cheaper price, simply to balance its exposure.

Furthermore, India has strengthened ties through mechanisms like the India-Japan-Australia Supply Chain Initiative, launched in 2021, which specifically aims to reroute supply chains for key sectors away from China. With Japan, India has an ongoing project to manufacture rare earth magnets, crucial for electronics and EVs, in India with Japanese support, an attempt to break China’s monopoly in that area. India is also actively participating in the U.S.-led Indo-Pacific Economic Framework, IPEF, notably joining the supply chain and clean economy pillars, while opting out of the trade market-access pillar for now. Through IPEF, India will collaborate on setting standards for digital trade, labor and environmental norms, which could eventually facilitate easier trade with the U.S. and allies, thereby reducing relative reliance on China.

In South Asia and the Indian Ocean region, India is offering itself as a development partner to countries that might otherwise turn to China’s Belt and Road Initiative. India provides lines of credit and builds infrastructure in Bangladesh, Sri Lanka, Mauritius, Maldives, Nepal, and African nations, seeking to create a network of trade and investment that offers a counter-weight to China’s economic influence. These efforts are as much about geopolitics as economics, but over time they could yield India new markets and sources. If neighbouring countries become stronger partners, India could import more from them, energy from Bhutan/Nepal, manufactured goods from Bangladesh, and export more to them, collectively diminishing China’s role in the region’s trade.

At the heart of India’s strategy is the drive for Atmanirbhar Bharat, or “self-reliant India.” The government recognises that the most durable way to reduce dependence on China or any single source is to build robust domestic capacity in critical sectors. We already discussed the ProductionLinked Incentive (PLI) schemes pumping subsidies into electronics, pharma, solar, autos, and more. Beyond PLIs, India has slashed corporate tax rates for new manufacturing to among the lowest in Asia, 17% effective, to attract investors. It has improved its ranking in the Ease of Doing Business index dramatically over the past decade by simplifying regulations, digitising approvals, and building physical infrastructure including highways, ports, and logistics parks, to support industry. All these efforts are meant to make India a viable manufacturing base where companies can produce at scale for both the domestic market and exports, thereby substituting what would have been imports from China.

Electronics manufacturing in India has boomed, with exports of cell phones jumping from near zero a few years ago to over $10 billion now. India is now the second-largest mobile phone producer after China, thanks to the PLI-fueled investments. Global contract manufacturers, Foxconn, and Pegatron, and Indian firms alike are assembling not just phones but also tablets, laptops with a new PLI in IT hardware underway, and wearables. The government is also nudging them to indiginse components such as making display modules and chip packaging in India, not just final assembly. One notable development, an Indian electronics firm, Dixon Technologies, recently formed a joint venture with China’s HKC to manufacture display screens in India. This indicates a pragmatic approach, if Chinese expertise is needed to build capability, bring it onshore under controlled conditions rather than continue imports. Similarly, in automotive, India’s Tata Group acquired a European battery company to start producing EV batteries domestically, aiming to curb future imports from China.

India’s famed pharmaceutical sector is being retooled to regain upstream self-sufficiency. The government has earmarked sites for bulk drug parks with common utilities where API makers can get cheaper power, water, and effluent treatment, cutting production costs to compete with China. The initial response from industry is positive, with multiple projects in progress. In renewable energy, Indian conglomerates are investing in integrated solar manufacturing from polysilicon to panels and in advanced battery gigafactories, backed by government incentives. These will take a few years to come on stream, but they hold promise to supply India’s green expansion from within, rather than via imports.

Another key prong is technology and innovation. India is pouring resources into R&D missions, from space and satellite tech, where India is strong and even exports to some degree, to cutting-edge fields like 5G/6G standards, quantum computing, and AI. Collaborations such as the U.S.-India initiative on emerging technologies, mentioned above, aim to give India access to Western knowhow, so it doesn’t have to rely on Chinese tech solutions. India is well on way to foster its own 5G core or source it from trusted partners, it won’t ever need Huawei. The same logic applies to AI and telecom software, India is working with the U.S. on Open RAN, open-source 5G architecture, which could provide a non-Chinese, interoperable path for telecom networks.

Pressingly, human capital and skill development are being ramped up. One advantage India holds is its large, youthful workforce, but to utilise it, the workforce must be skilled for manufacturing and high-tech jobs. Initiatives like Skill India are training millions of youth in trades like electronics repair, machining, coding, etc. This will gradually make India even more attractive as a manufacturing alternative to China, where the labor force is aging and wages are higher. A demographic dividend could make India the next workshop of the world in certain sectors, foreign companies already see that potential, which is why despite all odds, over 100 Chinese companies from Xiaomi to BYD were active in India in recent years, and many global firms are expanding India operations.

In the strategic sectors, India is also pursuing self-reliance with partnerships. Take defense, India has curtailed imports from all sources, including from Russia, and underlined making weapons locally, with foreign collaboration if needed. This extends to drones and cybersecurity products where Chinese options are off the table due to security, so India is indigenising those. In critical infrastructure like power grids, India now mandates testing of all equipment for malware, this arose after concerns that Chinese-made transformers could have embedded malware. India even developed its own alternative to China’s Belt and Road in collaboration with Japan, the Asia-Africa Growth Corridor, focusing on connectivity projects that align with Indian and Japanese standards rather than Chinese loans. While that specific initiative is still in early stages, it shows India’s intent to offer different models of engagement.

India’s external and internal strategies reinforce each other, by broadening its circle of trade partners, India reduces the overhang of any single partner, and by strengthening domestic manufacturing, it reduces the need for imports. This doesn’t mean India will stop trading with China, realistically, China will remain a top trade partner for the foreseeable future given its central role in global supply chains. But India is positioning itself so that this trade is on more balanced terms. As one report put it, the overlap between trade and national security is driving a resurgence of industrial policy worldwide, and India is no exception. New Delhi wants to trade with everyone, including Beijing, but without being vulnerable to pressure. If it can pull off this delicate balancing act, India will emerge more resilient and self-sustaining, able to engage China from a position of greater strength.

India-China trade interdependency will continue, but its nature is evolving in the shadow of strategic competition. Historical patterns of India as primarily an importer and China as exporter persist, yet India is no longer a passive player in this equation. Through diplomatic diversification, protective measures, and a manufacturing push, India is slowly recalibrating the terms of engagement. The coming years will test how far this rebalancing can go. A pragmatic scenario is one of managed interdependence, robust trade ties, but hedged by safeguards and supplemented by alternative partnerships. Both Asian giants have much to gain from economic cooperation, and indeed their trade has underwritten prosperity on both sides, but both are also acutely aware of the geopolitical undercurrents. The India-China trade story, much like their broader relationship, is one of cautious engagement, driven by economics, constrained by strategy. Maintaining this equilibrium will require deft management, lest economic compulsions clash with national security imperatives. The world, especially investors and policymakers, will be closely watching how India and China navigate this complex interplay in the years ahead, as it will shape not just their own futures, but the economic architecture of the entire Indo-Pacific region.