By Aarav Beniwal

Foreign investors have pulled more capital out of Indian equities in the first four months of 2026 than in all of 2025. The Nifty has barely flinched. A new ownership structure is rewriting how India’s market clears, and changing what foreign capital is worth to it.

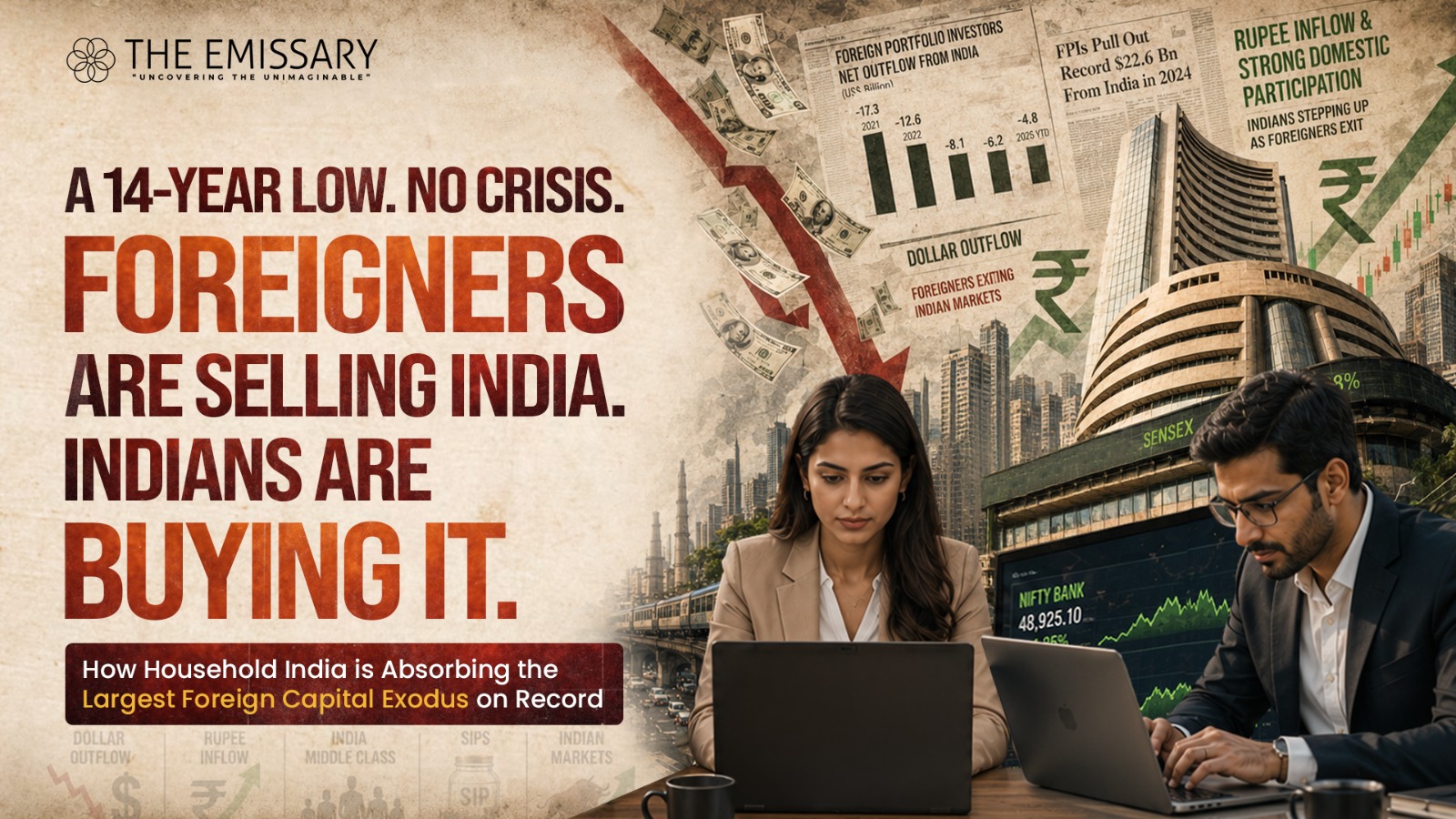

By every conventional metric, Indian equities should be in crisis. Foreign Portfolio Investors (FPIs), the institutional buyers of Indian stocks who sit outside the country and trade through offshore vehicles registered with the Securities and Exchange Board of India (SEBI), the capital markets regulator, have sold ₹1.92 trillion (around $22.5 billion) of Indian shares in the first four months of 2026, according to the National Securities Depository Limited (NSDL), the registry tracking foreign portfolio flows. That exceeds the ₹1.66 trillion FPIs withdrew in the entirety of 2025. In March 2026 alone, foreign selling reached ₹1.17 trillion, the largest single monthly outflow on record.

And yet the market has not broken. The Nifty 50, the National Stock Exchange’s benchmark index of India’s fifty largest listed companies by free float, fell 9.37% in March, its steepest monthly decline since the COVID-19 crash of March 2020. By mid-May it had largely recovered. The BSE Sensex, the older flagship index of the Bombay Stock Exchange covering thirty leading companies, finished 2025 up roughly 10% even as foreign capital fled. The collapse a previous generation of strategists would have predicted, an emerging market panic on the scale of 2008, has simply not arrived.

This is the Indian paradox of 2026, a record foreign exodus colliding with a market that refuses to capitulate. The reasons reveal a structural shift in who owns India Inc., and the verdict for investors is more complicated than either bulls or bears will admit.

Why the foreigners are selling

The selling has been neither random nor wholly negative for India. Four reinforcing global pressures have driven it.

First, the artificial intelligence trade. Since OpenAI’s commercialisation of large language models in 2022 reshaped global capital allocation, the marginal dollar of equity money has rotated toward US technology giants, and within emerging markets toward Korean and Taiwanese semiconductor firms that supply the AI hardware stack. India, whose Information Technology (IT) services industry is built on labour arbitrage in software development for Western enterprises, sits on the wrong side of that trade. In February 2026, even on a month when FPIs were net buyers in India overall, they pulled ₹16,949 crore out of Indian IT stocks alone. Over the twelve months to April 2026, JM Financial recorded $9.22 billion of foreign outflows from Indian IT.

Second, valuation. The Nifty 50 trades at a forward price to earnings (P/E) multiple of around 22, against roughly 13 for the MSCI Emerging Markets Index, which is the Morgan Stanley Capital International benchmark covering large and mid-cap stocks across 24 developing economies. A premium for Indian growth has always been justified. A 70% premium becomes harder to defend when earnings momentum slows and global liquidity tightens.

Third, the US yield curve. The yield on the United States 10-year Treasury, the global riskfree reference rate, has been testing 4.5% through early 2026. For a dollar-based allocator, owning safe US government paper at 4.5% sets a high bar for any emerging-market equity to clear after currency risk. The Indian rupee, meanwhile, has weakened past ₹92 to the dollar, eroding dollar-denominated returns even before any move in share prices.

Fourth, the China alternative. After years of underperformance, Beijing’s stimulus packages and the relative cheapness of Hong Kong-listed Chinese stocks have drawn emerging market funds back. The Hang Seng Index posted a year-to-date return above 23% in early 2026 against a roughly flat Nifty.

The cumulative result, captured by ownership data from the National Stock Exchange, is striking. FPI ownership of NSE-listed companies has fallen to 14.7% in April 2026, its lowest level since June 2012, according to JM Financial. A decade ago in April 2016, that share stood at 19.9%. India has been steadily de-foreignising for a decade, and the process accelerated sharply in 2025 and 2026.

The domestic cushion

What has replaced the missing foreign bid is the quintessential development in Indian capital markets since liberalisation in 1991, and it is the reason the market has not collapsed.

Domestic Institutional Investors (DIIs), a category that includes mutual funds, life insurance companies, most prominently the state-owned Life Insurance Corporation of India, pension funds, and banks investing on their own books, now own 18.9% of NSE-listed firms. That is more than FPIs for the first time in modern Indian market history. Crucially, in March 2026, when foreigners sold ₹1.17 trillion, domestic mutual funds alone bought a record ₹1.05 lakh crore, about $12.3 billion, of Indian equities, and total DII buying reached ₹1.43 trillion. JM Financial’s analysis found DIIs increased their stake in 39 of the 41 Nifty 50 stocks that FPIs were selling. Where foreigners exited, domestics absorbed, almost one for one.

The mechanism is the Systematic Investment Plan (SIP), an Indian retail product offered by mutual funds that auto-debits a fixed monthly amount from an investor’s bank account and routes it into a chosen scheme regardless of market level. SIP contributions reached ₹32,087 crore in March 2026, up 7.5% month on month, even as headlines screamed about the foreign exodus. Total SIP assets stood at ₹15.10 lakh crore, equal to 20.5% of the mutual fund industry’s total Assets Under Management (AUM, the standard measure of money managed by a fund or industry).

The aggregate has compounded into something structural. The Indian mutual fund industry’s AUM stood at ₹73.73 lakh crore on 31 March 2026, almost six times the level of March 2016. Equity mutual funds posted net inflows for the 61st consecutive month, a streak dating to March 2021. Combine the 9.5% direct retail ownership of NSE-listed firms with the mutual fund share that households indirectly hold, and individual Indian investors now own 18.75% of the market, a 22-year high, according to NSE data.

This domestic float is what allowed the Nifty to fall 9% in March rather than 30%. A market that would have crashed under comparable foreign selling in 2008 simply went sideways in 2026.

The structural reasons behind the cushion

Three drivers explain the rise of the Indian retail investor as a market-clearing force.

The first is demographic and technological. India now has roughly 13 crore (130 million) demat accounts (dematerialised securities accounts, the electronic ledgers in which Indian shareholders hold their shares), up from 4 crore in March 2020. COVID-era digital onboarding combined with Aadhaar-based Know Your Customer (KYC) verification, the biometric ID-linked compliance regime, pulled millions of first-time investors into equities during the lockdown savings glut.

The second is regulatory. SEBI has spent the past three years tightening derivatives rules and clamping down on speculative single-stock futures and options trading. The consequence has been to channel more retail capital into long-only mutual funds and Exchange Traded Funds (ETFs, passively managed funds that track an index and trade like shares).

The third is fiscal. Real interest rates on bank fixed deposits, the traditional Indian savings instrument, have been negative or flat for much of the post-pandemic period. Small-savings products such as the Public Provident Fund (PPF, a government-administered long-term tax-free scheme) have lost relative appeal as equity returns have compounded. The result is the “financialisation of household savings”, a generational reallocation from gold and property into financial assets that, on every penetration metric, still has years to run.

Where the cushion has limits

The resilience is real, but it is not unlimited. The first warning is concentration. Foreign selling has been heavily focused on three sectors of disproportionate index weight: Information Technology (IT), Banking, Financial Services and Insurance (BFSI), and Fast-Moving Consumer Goods (FMCG). The twelve-month FII flow data shows net selling in ten of sixteen sectors. The BFSI sector alone saw $6.49 billion of outflows in March 2026. Because BFSI accounts for roughly a third of Nifty weight, even substantial domestic buying cannot fully compensate at the index level if foreign selling in this segment continues at the current pace.

The second is valuation. Nomura’s India equity strategist Saion Mukherjee has contended, India’s premium over other emerging markets has narrowed to “more normal levels” only after the recent correction. If domestic flows continue to absorb foreign selling at current prices, the premium may re-widen; and if global allocators see India trading at rich multiples while growing slower than they had expected, the marginal foreign seller stays a seller.

The third is macroeconomic. India imports about 85% of its crude oil. Brent crude prices crossed $100 a barrel in early 2026 on West Asia tensions. If they remain there, India’s current account deficit, which is the gap between what India pays foreigners for imports and what it earns from exports, inflates, the rupee weakens further, and the Reserve Bank of India (RBI), the central bank, has less room to cut interest rates, which corporate earnings now need. The cushion is a function of household savings flows, and those flows depend on macro stability. A sustained oil shock or rupee crisis would, at some point, slow SIP growth.

The fourth is behavioural. SIP investors have so far behaved with remarkable discipline. But most have not experienced a deep, sustained bear market in their investment lifetimes as the majority of demat accounts were opened after March 2020. The real test will come not when the Nifty falls 10% in a month, as it did in March 2026, but when it falls 20% and stays down for a year. There is no historical Indian data for how a retail base of this size behaves in that scenario.

The debt counter-narrative

The equity exodus has obscured a parallel and more positive story in Indian government bonds.

In September 2023, JPMorgan Chase announced that Indian government bonds issued under the RBI’s Fully Accessible Route (FAR), a framework that allows foreign investors to buy specified government securities without quotas or repatriation limits, would be added to its Government Bond Index Emerging Markets (GBI-EM), the world’s most widely tracked emerging-market debt benchmark. Inclusion completed in March 2025 at the maximum 10% weight, placing India alongside China, Indonesia, and Mexico.

Between the September 2023 announcement and the June 2024 inclusion start, monthly debt FPI flows into India averaged ₹11,500 crore, against a combined ₹49,000 crore for the three years before the announcement. The Bloomberg Emerging Market Local Currency Government Index and FTSE Russell’s Emerging Markets Government Bond Index added India in subsequent months, each expected to bring incremental flows of $2 billion to $3 billion. By late 2025, FPIs had net bought roughly ₹27,567 crore of Indian debt even as they were selling equities, drawn by 10-year Indian government bond yields near 6.5% against US Treasury yields around 4.5%, a spread that compensates for currency risk over the medium term.

The debt tale matters because it represents what the equity one does not: a structural, index-mandated foreign bid that does not depend on India winning the AI trade. It also helps explain why, despite headline equity outflows, India’s balance of payments has held and the rupee, while weaker, has not entered free fall.

How investors should judge this

For investors, the implications fall into three buckets. For foreign allocators, the question is whether to call the bottom in India’s underperformance. Nomura projects the Nifty 50 will touch 29,300 by end-2026, an upside of about 13% from mid-May levels; HSBC forecasts the Sensex at 94,000, an 11% rise. Both rest on assumptions that earnings downgrades have run their course and India’s premium has corrected to defensible levels. The trade, however, is selective rather than index-wide. Capital goods, where FPIs have been net buyers every month of 2026 on the India capex story; financials at lower valuations, where steady credit growth supports earnings; and consumer discretionary including autos, which benefits from monetary easing as the RBI cut its policy repo rate by 50 basis points in mid-2025 and the Cash Reserve Ratio by 100 basis points, are the segments where foreign conviction remains intact. The bet is on India’s investment cycle, not its index multiple.

For domestic investors, the lesson is more perturbing. The mutual fund industry has not been tested in a prolonged drawdown, and many SIP investors have only known a one-way market since they began. The right behaviour, paradoxically, is to keep doing what produced the cushion, continue SIPs through the volatility, accept that index returns will be lower than the past decade as the premium normalises, and avoid concentrated bets on sectoral funds (especially IT-only schemes) where the AI rotation is structural and not cyclical. Flexi-cap and multi-cap funds, which allow managers to rotate across market caps, are better suited to an environment in which sector leadership is changing faster than retail can track.

For policymakers in New Delhi, India’s resilience is not a signal that foreign capital does not matter. FPI outflows have already pushed foreign ownership to a fourteen-year low; the domestic buffer is large but not infinite. Sustaining global investor interest requires what foreign allocators have long said they want and what India’s reform record has only intermittently delivered: predictable tax policy, faster contract and dispute resolution, less retroactive regulation, and a credible promise that the next Vodafone retrospective tax case or Adani-style governance shock will be handled transparently. The proposed India-US trade deal, still unfinalised at the time of writing, is the most immediate test of that signalling. Resilience earned by household India is a precious form of capital. It is the wrong base on which to grow indifferent to foreign re-engagement.

What the paradox means

The Indian paradox of 2026 is, in the end, a story of who absorbed the punch. Household India did, through 130 million demat accounts and a ₹32,000 crore a month SIP machine that did not flinch when foreign capital ran. The market that emerges on the other side will be slower growing than consensus once anticipated, less foreign-owned than at any point this century, and more leveraged to the discipline of a retail base that has yet to be tested by a deep, sustained bear market.

The right question for investors is no longer whether India can survive an FPI exodus. The past four months have answered that. The right question is what kind of market India becomes when its domestic float is structurally larger than its foreign one, when valuations are set at the margin by ₹500 SIPs from Tier-3 cities rather than by sovereign wealth fund allocations from Singapore, and when global capital that does return must price itself against a domestic bid that no longer treats it as the marginal buyer. And how and in what ways could that grow?

That is a different market from the one foreign investors learnt to trade in the 2010s. It is also, as the 2026 selloff has just demonstrated, a more resilient one. The cost of that resilience, in lower returns and slower convergence to developed-market valuations, is what the next two years will reveal.